Walk into the control room of any MENA refinery, gas treatment plant, or upstream facility built between 1995 and 2015 and you will find the same thing: a distributed control system from Emerson, Honeywell, ABB, Siemens or Yokogawa, an asset management system layered on top, a proprietary communication bus that nobody on the local team fully understands, and a support contract that renews every three years for roughly the cost of a new mid-sized control system.

The cost of change is deliberately high. The vendor owns the engineering tools, the driver libraries, the device type managers, the historian schemas, and the spare-parts supply. Any modification that is not on their roadmap gets priced as a project. Any integration that competes with their own product gets quietly locked out. This is not a conspiracy — it is a business model. It has worked brilliantly for the vendors and it is now breaking under the weight of every digital transformation initiative in the region.

This brief is the engineering view from a team that has migrated industrial automation architectures from vendor-locked DCS and AMS environments to independent PLC-based systems that the operator actually controls. It explains why the migration is now unavoidable, what the independent architecture looks like, and where the real savings hide.

The vendor lock-in that runs MENA industry

The proprietary DCS is the quiet king of process automation across the Maghreb and the Gulf. Sonatrach's upstream and midstream assets, the Algerian refineries, the Saudi petrochemical complexes, the Emirati gas treatment plants — the vast majority are running control systems where the engineering workstation only speaks to devices through vendor-signed drivers, where the historian is locked to the vendor's schema, and where adding a simple third-party flow meter to the asset management loop costs more in licensing than the meter itself.

Asset management systems are the worst offender. AMS Device Manager, FieldCare, PRM — all of them were designed in the HART-protocol era to centralize device configuration and diagnostics, but the vendor priced the architecture so that the cheapest path to add or replace any instrument is to buy more of the same vendor. The handbook says open protocols. The practice says a minimum of 60% vendor-branded hardware in the loop or the calibration tool refuses to load.

For an operator sitting on 15,000 field instruments, 400 control loops, and a twenty-year remaining asset life, this is a serious strategic problem. It is also the problem that every MENA national oil company is now being told to solve by 2030 as part of their digital transformation mandate.

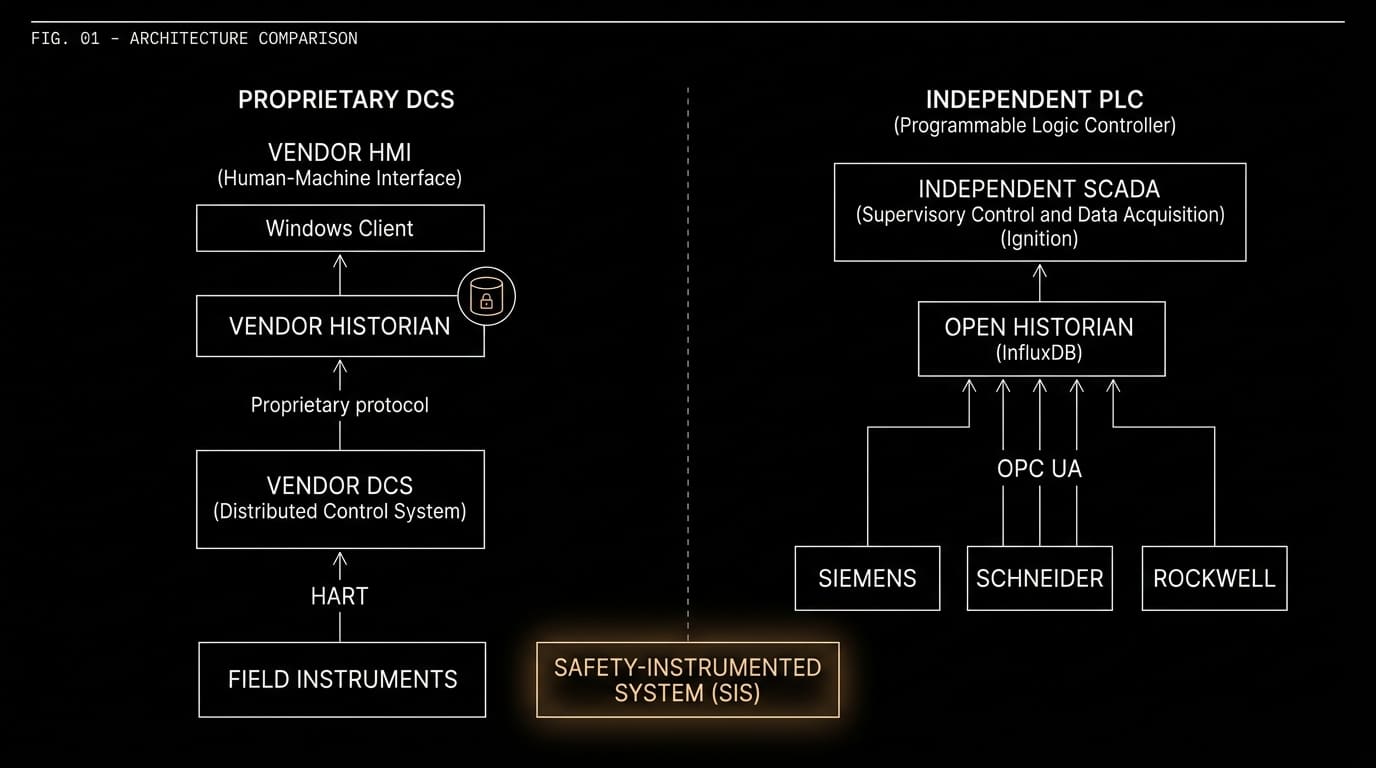

What independent control actually means

The alternative is not to rip out the DCS. The alternative is to put the decision layer — the PLCs, the supervisory layer, the data layer, the analytics layer — on open architectures that the operator owns. The DCS becomes an execution layer for safety and interlock logic where it still makes sense. Everything above it becomes vendor-neutral.

In concrete terms: Siemens, Schneider, Rockwell, Beckhoff, or Bachmann PLCs connected via OPC UA instead of proprietary protocols. Historian layer on InfluxDB or TimescaleDB instead of a locked vendor database. SCADA on Ignition, Zenon, or a custom React-based HMI instead of the vendor's 2008-era Windows client. Asset management on FDI-standard device descriptions instead of vendor-only device type managers. Everything above the safety-instrumented system becomes replaceable, upgradable, and independent.

The engineering team inside the plant can now modify loops without a licensing call to Europe. The spare-parts inventory can source from three different vendors at competitive prices. The historian can feed a predictive maintenance model, a cost controller, or a regulatory report without a $200,000 data-integration project each time.

The economics — where the savings actually come from

The first misconception about this migration is that the savings come from cheaper hardware. They do not. A Siemens S7-1500 is not meaningfully cheaper than an Emerson DeltaV controller. The savings come from three other places.

License freedom — not having to pay $2,000 per engineering-workstation seat per year, not having to pay per-tag licensing on the historian, not having to pay the vendor's certified integrator $1,800 per day to do work your own team could do with a published API. Across a mid-sized refinery, license-freedom alone is $500,000 to $2 million per year, depending on the installation.

Vendor competition on instruments — when the loop is open-protocol, a Yokogawa flow meter, an Endress+Hauser pressure transmitter, and a Rosemount level gauge all work equally well in the same configuration environment. Prices drop 15 to 30% on the instrument line item over a five-year procurement cycle. For an operator buying 500 to 2,000 instruments a year, this alone funds the migration.

Unlocked data — this is the one that actually matters. The process data that sits in a vendor historian today is worth between $1 and $5 per tag per year when it is free to feed predictive maintenance, yield optimization, energy reconciliation, and environmental reporting. For a 50,000-tag facility, that is $50,000 to $250,000 per year of value that is currently locked inside a proprietary schema because the vendor wants to sell their own analytics suite on top.

The OT/IT convergence problem nobody solves cleanly

The reason these migrations fail more often than they succeed is that they are run by IT departments that do not understand safety-instrumented systems, or by OT departments that do not understand modern software architectures. The successful migrations are run by teams that operate both sides fluently.

OT-side requirements that IT teams routinely miss — deterministic response times below 50ms for critical loops, proper safety integrity level (SIL 2 / SIL 3) segregation between control and safety layers, hot-standby redundancy with seamless failover, 10-to-20-year component availability, proper handling of IEC 61131-3 programming standards, and the fact that a bad firmware upgrade can shut down a facility for three days and cost millions.

IT-side requirements that OT teams routinely miss — source control for PLC programs (not just the latest file on a USB stick in the engineer's drawer), automated testing of control logic, configuration-as-code for the SCADA layer, proper identity management and audit logging on every engineering change, network segmentation according to IEC 62443, and the ability to deploy a change to fifty identical pump skids without walking to each one with a laptop.

A team that does only OT will ship an architecture that is safe and unmaintainable. A team that does only IT will ship an architecture that is elegant and unsafe. The team that does both is rare — and it is exactly what MENA national oil companies now need to find.

The migration playbook — what actually works

If you run a refinery, gas plant, or chemical facility in Algeria, Saudi Arabia, the UAE, or anywhere else in the region and want to move away from vendor lock-in without rebuilding the plant, the sequence is now well-understood.

Phase one: instrument the data layer, do not touch the control layer. Install an open historian (InfluxDB / TimescaleDB) in parallel with the vendor historian. Feed it from the existing DCS through OPC DA / OPC UA gateways. Keep running the plant exactly as before. This phase alone unlocks 80% of the data value without a single risk to production. It typically pays for itself within twelve months from the analytics use cases it enables.

Phase two: migrate the supervisory layer. Replace the vendor SCADA with an independent one (Ignition, Zenon, or custom) running alongside the existing one. Operators can run both for a transition period. The engineering ownership of the HMI shifts from vendor to operator.

Phase three: migrate non-critical control loops to independent PLCs. Utility systems, auxiliary pumps, material handling, metering skids — systems where a controlled shutdown is not a plant-wide event. This phase is where the team learns to engineer on the new stack under real plant conditions.

Phase four: migrate primary control, preserve safety. Core process loops move to independent PLC controllers. The safety-instrumented system stays on a certified SIL 3 platform — but it can be a competitive one, not locked to the DCS vendor. The asset management layer is rebuilt on FDI standards and open device descriptions.

Done in this order, the migration is a three-to-five-year program with measurable ROI at every phase and zero heroic cutovers. Done out of order, it becomes a rip-and-replace that threatens production.

Why MENA is the right place to do this right now

Three things make 2026 the right moment. First, the major vendors have exhausted their pricing leverage — their software maintenance fees have risen faster than inflation for a decade and operators have finally started to push back with budget-approved migration projects. Second, open-protocol support on the instrument side has matured to the point where interoperability is no longer a lab demonstration; it is a procurement reality. Third, the MENA digital transformation mandates — Algeria's digitalization plan, Saudi Vision 2030, UAE Smart Industry, Qatar Vision 2030 — all now explicitly require vendor-neutral architectures in their new-build specifications.

The operators who start the migration now, phased correctly, will have a stable independent architecture by 2030. The operators who delay will hit the Vision-2030 compliance walls with a plant still running on 1998 proprietary DCS — and at that point the migration becomes emergency, not strategic.

This is the window. It closes around 2028.